“Obvious” is the most dangerous word in mathematics.

E.T. Bell

“Not everything that can be counted counts, and not everything that counts can be counted.”

Albert Einstein

By closing arguments the prosecution’s narrative had been stripped of any certainty as to

- WHERE the murders took place;

- WHEN they happened;

- or exactly HOW they were carried out.

That left: WHO-did it and WHY they did it.

San Bernardino County District Attorney Britt Imes admits to as much in his closing statement. (Click link below)

Prosecutor Closing Statements: Part 1

And to “prove” the WHY prosecutors built a theory primarily off two pieces of evidence.

- A cryptic email sent by victim Joseph McStay Sr. to Chase Merritt at 11:42 AM on February 1, 2010

- And quirky Quickbooks activity that (sort-of) began that same day at 12:24 PM. (Except Joseph McStay had tweaked Quickbooks in December of 2009 and January of 2010.)

The Prosecution’s Theory

The prosecution’s theory is that Joseph McStay sends the above email on February 1, 2010 at 11:42 AM. This email constitutes a demand for payment of 42K. Upon receiving this Chase Merritt stops everything he is doing (does not phone Joseph McStay to challenge the debt) but instead decides to commit check fraud, initiating this plan at 12:24 PM.

Merritt is alleged to have signed onto the CUSTOM side of Joseph McStay’s QuickBooks account a half hour after that email is sent. (McStay had two accounts with QuickBooks-“CONTACTS” & “CUSTOM”. Custom was the account for fountains McStay designed and built with Merritt)

It is speculated (never proven) by the prosecution that Chase (not Joseph) adds Merritt as a vendor to the “CUSTOM” account. And if you believe it is Chase performing these activities, he drafts a check to himself, but does not print it. He then deletes it from the log.

We’ll put aside for the moment that we don’t know when Chase Merritt actually reads this email (he had a flip phone absent internet access), but if the email is his trigger to commit sudden check fraud, a half hour seems an incredibly short span of time to come up with this plan. Chase has to do more than simply sign onto QuickBooks. He has to acquire the necessary computer checks, and then deposit these checks without Joseph noticing. Joseph was constantly monitoring the flow of money in and out of his EIP bank account, he had to in order to know when payments could be made to vendors like Chase and Metro Sheet Metal. (Impulsive doesn’t even begin to cover it.) There is no evidence of Merritt initiating any activity on Joseph’s QuickBooks before this time.

But there is evidence of Joseph McStay making changes to both his Contacts and his Custom accounts, starting in December of 2009, and then again in January of 2010. In fact, Joseph McStay begins, for the first time generating computer checks (as opposed to handwriting them as he previously done).

He also adds Chase to the Contacts side as a vendor and adds two new vendors to the Custom account on January 25th.

AND DA Imes neglects to mention that there is also payment due Chase referenced in the email.

Giving DA Imes the benefit of the doubt, that his interpretation of the email is at all correct, and that Joseph McStay is demanding immediate payment from Chase, Joseph would then certainly have to deduct what he owed Chase from what Chase owed him That’s 42K – 26K = 16k.

So if there were a demand for payment, it would actually be-

$16K NOT $42K

Still a lot of money, but as Forensic Accountant Dennis Shogren testified to, Joseph and Chase had this kind of debt between them throughout their entire working relationship. At times Chase owed Joseph, other times Joseph owed Chase. See below. They each owed the other as much as 20K at times, so 16k hardly seems like a deal breaker for either man.

One completed project, like the Saudi Arabia deal (see below), could have more than covered that $16K debt. And all indications are that the start of 2010 was looking good for Earth Inspired Products (EIP).

Again, DA Imes never attempts to answer two critical questions:

- When did Chase actually READ that email? (This is relevant, because if Chase didn’t read the email until later that night, there is no incentive for him to suddenly begin writing fraudulent checks to himself.)

- Was it even characteristic for Joseph to demand immediate payment from anyone?

And what incentive is there for Joseph to demand payment immediately?

Joseph knows that Chase has a family to support, so even if payment was due relatively soon, the two men had many ways to work out a payment plan. One in keeping with how money had flowed between them for all three years they worked closely together.

Testimony of Forensic Accountant Dennis Shogren Part 2

So if there is no immediate demand for payment, what incentive is there for Chase to suddenly steal from a man who he is scheduled to make a great deal of money with in the upcoming year? What possible reason could he have for doing this, even if he had read the email the minute it came?

Below is a text that Joseph McStay sent to Chase Merritt on January 3, 2010.

What evidence is there that anything altered between these two men, so dramatically that suddenly a month after this text is sent, Chase would then be compelled to kill Joseph and three others? Two of whom were children, close in age to his own? Is the answer in the QuickBooks activity?

Prosecution’s Theory Continued

The state’s theory then builds on this unexplained QuickBooks activity. According to investigators and the prosecution:

- Chase, on receiving the “demand-for-payment” email, initiates QuickBooks fraud on February 1-he doesn’t write a check, only enters the program and tests it; on February 2 he writes a check, cashes this (important to note that the morning of the 2nd, Chase is in Fallbrook, and travels directly home, initiating the QuickBooks activity then-almost as if Joseph had instructed him to). And with a hand-written check given him by Joseph on that same day, opens a new account at Bank of America.* this handwritten check is likely significant, but more on this later.

- On the morning of February 4 Joseph McStay is thought to sign onto the CUSTOM Quickbooks account..

- It is what Joseph sees on QuickBooks that prompts him to make a lunch appointment with Chase.

- Joseph then calls his bank for the first time that quarter.

- All this, the state contends, supports the theory that Joseph fired Chase at the lunch meeting in Rancho Cucamonga at Chikfila

- And that four hours after being fired, and after receiving 7 more calls from Joseph that afternoon (one of which occurred while Joseph sat at his desktop computer looking over a design they had been working on since Sunday) Chase murders an entire family…because he was fired.

Hiccups…

- Problem is that Joseph could not have opened QuickBooks that morning, he was already midway to Rancho Cucamonga when Quickbooks was opened twice, briefly. At 11:56 & 11:57 AM.

- The person most likely to have opened the program briefly is Chase. And likely this was done in preparation for his meeting shortly with Joseph.

- So there is no sudden discovery of theft by Joseph that morning.

- Also Joseph spoke with his father that morning at around 10 and told him then of his lunch meeting with Chase and did not seem worried about anything.

- So Joseph clearly DID NOT arrange this meeting on the discovery of some type of nefarious activity on QuickBooks. (If the state has it right, Joseph hadn’t opened the CUSTOM account all week.)

- Joseph didn’t phone his bank for the first time that quarter on February 4. He had, in fact, phoned his bank twice the day before on February 3rd.

- Joseph also calls Chase seven more times after their meeting.

- Why would Joseph continue to call a man he had just fired?

- Joseph’s pings have him at home by 4:18PM when he gets immediately onto his desktop computer, opens the design program SkectchUp to a water feature he is planning with Chase, and then CALLS CHASE

Here’s what Joseph doesn’t do:

Joseph does not change his QuickBook’s password

Joseph does not call his bank to alert them of fraud

Joseph does not call another welder to fill in for the recently “fired” Chase

What the????

It is the fact that there was no activity by way of a computer in the McStay home at the time the February 1 QuickBooks activity takes place, that is the lynchpin to the state’s case. The prosecution’s assertion is that all the QuickBooks activity on the CUSTOM account, from February 1 on (even that which is documented to occur on Joseph’s desktop computer), is performed by Chase Merritt either via a computer he had access to at his residence, or on February 4, via Joseph’s desktop EMachine.

The question I would imagine everyone has, is, if there was no computer activity on McStay computers on February 1, from what computer then did Joseph McStay send the 11:42 AM email? Because the state does not claim that Chase Merritt wrote that email.

")

More Questions:

- If law enforcement failed to find the computer Joseph sent the 11:42 AM email from, could that email have been sent from the missing laptop, “Joseppe”?

- And if the email was sent from the missing laptop, maybe the check writing was performed from that computer as well…

What’s going on?

So what the heck was going on with Joseph, Chase and that cryptic email and Quickbooks? To explore this, the easiest path to follow is the prosecutions, because it is that narrative on which this speculation is based. And the theory is speculative. No one has ever claimed to know precisely what Joseph McStay meant in that email. The state’s contention is that Joseph sent the email to Chase to demand payment of 42K. Here are the problems I see with this assumption:

- The amounts noted on the email are both current and historic: Paul Mitchell (PM) & Saudi Arabia (SA) were current, on-going projects being paid out to Chase at the time of the email being sent. Levine & Provecho are projects from 2007 & 2008 where there was a problem with payment from the client, and the legal outcome was in question.

- Headings like “Savings” are not explained, and none of the numbers given are 15% of either the PM or SA totals (Amounts listed are actually 25% & 50% of the total invoiced on mentioned projects – see analysis below.)

- If we can’t be certain of the headings, or why old debts are commingled with new, how are we to be certain of any interpretation?

Plausible

Here is a possible explanation for what is occurring in this cryptic email.

There is either a typo or Joseph doesn’t take his headers all that seriously. The percentage seen is not 15% it is 25% – 50% depending on what the project is, and how much of the invoice has been paid by the client.

- The Saudi Project-SA (see invoice below), if rounded off is actually 57K (minus installation).

- Per the email: 14,225—-which is about 25% of the total project (57K x 25% = $14,250). Amount in email is just $25 shy of the exact 25%. (7725 + 6500 =14,225)

- Only half the deposit was paid by the client. When second half of payment comes in from client it seems likely that Chase is going to see another 14K on this project or part of this amount, some percentage going to Metro Sheet Metal.

- Chase had spoken of a 65/35 split with Joseph on projects. This breakdown is apparent with the Saudi Project.

- Chase will be paid 28K total (once the invoice is paid in full).

- And Metro Sheet Metal is paid 9K for the initial bending of the metal involved (see below)

- The combined payments to Chase and Metro are approx. 37K

- Joseph receiving 20K, which is about his usual 35 percent.

- Basically it appears that the breakdown on all of these projects, is always in the ballpark of: 65% went to manufacturing-Chase & Metro / 35% went to Joseph McStay.

- Depending on how much Metro was paid, Chase basically made the rest. And this likely changed from project to project.

- *Installation fees mentioned appear to have been paid on top of the cost of the actual fountain, so installation fees do not factor into the percentages allotted.

- In regard to the Paul Mitchell project referenced:

- Chase is promised: $4000 & $3050=$7775

- 8K would be 50% of the PM project, $7775 is close, so in the email Joseph appears to referencing ALL the money Chase will make for that project. There are indications that by the time of this email Joseph had received full payment for the PM fountain (see below).

PM")

A brilliant plan….

But let’s say that DA Imes got it right. That Chase upon receiving that email is so incensed that rather than phone Joseph and challenge the debt, or ask for more time, Chase decides instead that it’s a better idea to commit fraud in a way he is absolutely certain to get caught.

Brilliant plan! Because though QuickBooks makes it possible to write a check on the bank account of another person (if you have the proper check) and to even cash or deposit that check gaining access to the money, once the check clears, the person whose account it is, will see that the money is gone. For clarification, QuickBooks is not the same as a debit card or credit card, or direct access to a bank account. It is basically an electronic checkbook.

This brilliant plan could only have been sustainable for a few days, tops! Joseph appears to have monitored his bank account pretty closely. He had to keep up with payables and receivables on an almost daily basis.

But lets just say, this IS what happened. Perhaps examining what the QuickBooks activity actually was, will help bring some elucidation to the matter.

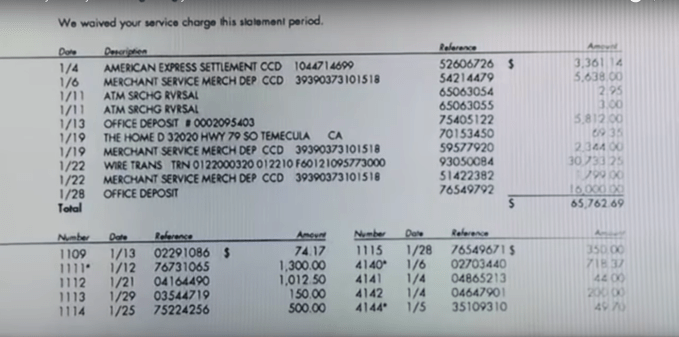

The sign-in and password used to access Joseph McStay’s CUSTOM account on the days listed below are the same that Joseph had always used. And as a reminder, Joseph McStay had two QuickBooks accounts. CONTACTS-an account he used for invoicing and paying both EIP and personal bills. And CUSTOM, which was specific to his work with Chase Merritt.

- December 2009: Joseph McStay suspends his QuickBook’s CUSTOM account, only to reestablish it a few days later.

- January 2010: Joseph McStay adds vendors to the CUSTOM account and adds Chase Merritt to the CONTACTS account. He begins to draft computer generated checks for the first time.

- February 1: “chase merritt” added as vendor (all lower case).

- Check written, payable to “chase merritt” ($2,500-this figure amount may prove to be important).

- Check deleted, not printed.

- Not performed via any McStay computer in evidence.

- Check written, payable to “chase merritt” ($2,500-this figure amount may prove to be important).

- February 2:

- Check written, payable to “chase merritt” ($2,495). Check printed. Chase cashes this check that day at branch of Joseph’s bank-Union Bank.

- Not performed via any McStay computer in evidence.

- Check written, payable to “chase merritt” ($2,495). Check printed. Chase cashes this check that day at branch of Joseph’s bank-Union Bank.

February 2 : Ping Evidence presented by Kevin Boles shows Chase at the McStay residence in the morning and then returning to Rancho Cucamonga at the time the check is drafted on CUSTOM to Chase. This timing is in keeping with a narrative of Chase picking up a blank check from Joseph, and then returning home to see if he can successfully draft and print a check. If Joseph only gives Chase one check that day, this would necessitate Chase getting more blank checks on the 4th.

Kevin Bole’s Ping Maps for Chase Merritt on February 2, 2010

District Attorney Imes, in his closing stated that the each piece evidence cannot be understood in isolation, the evidence must be examined within the larger context of all events occurring around it. So why didn’t he follow his own advice? He presents the email and the QuickBooks activity completely out of context with all the other related activity occurring at that time.

The addition of vendors to CUSTOM and the initiation of computer check writing from QuickBooks began in the month prior to the McStays going missing, and we know these actions were performed by Joseph, so why would it just be assumed that someone other than Joseph entered in “chase merritt” as a vendor on Feb 1?

February 1 QuickBook’s entries begin a half hour after the 11:42AM email is sent. Joseph’s phone log shows that he could easily have been multi-tasking at the time. And again, if we don’t know what computer the email was sent from, yet we know Joseph sent that, the QuickBooks activity could just as easily have been performed by Joseph at the computer from which he sent the email.

Which if one were to take a stab at an educated guess, is the missing “Joseppe” computer.

Viewing the phone calls Joseph is making and the when the email is sent, it would appear he was alternating between computer work and making calls. The 11:42 email is sent smack dab in between two phone calls. And right after the QuickBooks activity is completed, Joseph calls Chase.

It makes much more sense, given the timing of the email to the QuickBooks activity, that this is Joseph, rather than Chase doing this. A half hour is a remarkably short time period for a man to suddenly decide to commit check fraud over a 16K debt. (A debt easily reconciled sans fraud.)

But a half hour is not that long a time span from sending an email, and then engaging in other computer activity.

***

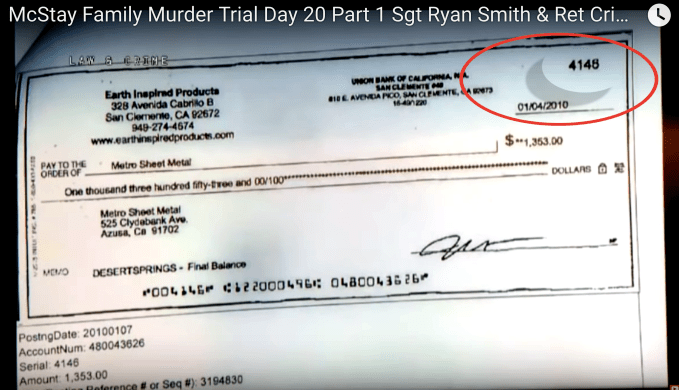

The checks, though they appear out of sequence, are actually in sequence, but by project, not by date. And it would seem that Joseph decided to write his computer checks by way of the 4100 series, giving checks from the 4200 series to Chase. This might have allowed Joseph to know right off who had written the check, and this way he could easily verify that the amounts were correct.

Most of this post references events at trial, but the search warrants are helpful in getting some clarification. Below is SBSW 14-1590–

What is clear is that the in terms of known behavior, the QuickBooks activity on February 1, 2010 is more consistent with Joseph McStay’s past QuickBooks activity (and QB activity verified to be his, near to the time of his death), than it is with Chase Merritt suddenly, within a half an hour of receiving an email, deciding to commit check fraud.

There is an order to how the checks were written between February 1 & 8, on the CUSTOM side of Joseph McStay’s QuickBooks account that is, again, more consistent with Joseph McStay’s methods – than that of someone attempting to embezzle. It would appear that Chase was following Joseph’s explicit instructions, rather than as the SBC DA wildly speculates, engaging in some type of sudden, inexplicable and ineffective embezzlement scheme.

Which means that the February 1st and 4th, QuickBooks activity is also more consistent with Joseph McStay being at his own computer, futzing with QuickBooks, than Chase Merritt opening the program directly after receiving an email or directly following the bludgeoning of four people to death–driving away with them in a truck, then somehow returning to the home less than ten minutes later-to write a check he doesn’t print, and could have written from a safer, easier location.

There, unfortunately, will never be any way to verify exactly why Joseph at the end of 2009 and start of 2010 began writing computer checks, rather than hand drafting them as he had previously done. Or why Joseph wanted to take the CUSTOM account offline and directed Chase to write checks to himself, taking care of payment due him on the custom water features the two built together. And we may also never know why Joseph wanted Chase to take care of the mundane task of transferring the CUSTOM account to desktop, rather than taking care of this himself, but it is clear that this is what occurred.

In conclusion, there is order to the appearance of Chaos in the check writing. What is apparent in actions by Joseph around the time of this new check writing, is that he was not only altering the use of the CUSTOM account, but how he wrote checks in general.

You must be logged in to post a comment.